Course info

Course Summary: Numerical Methods

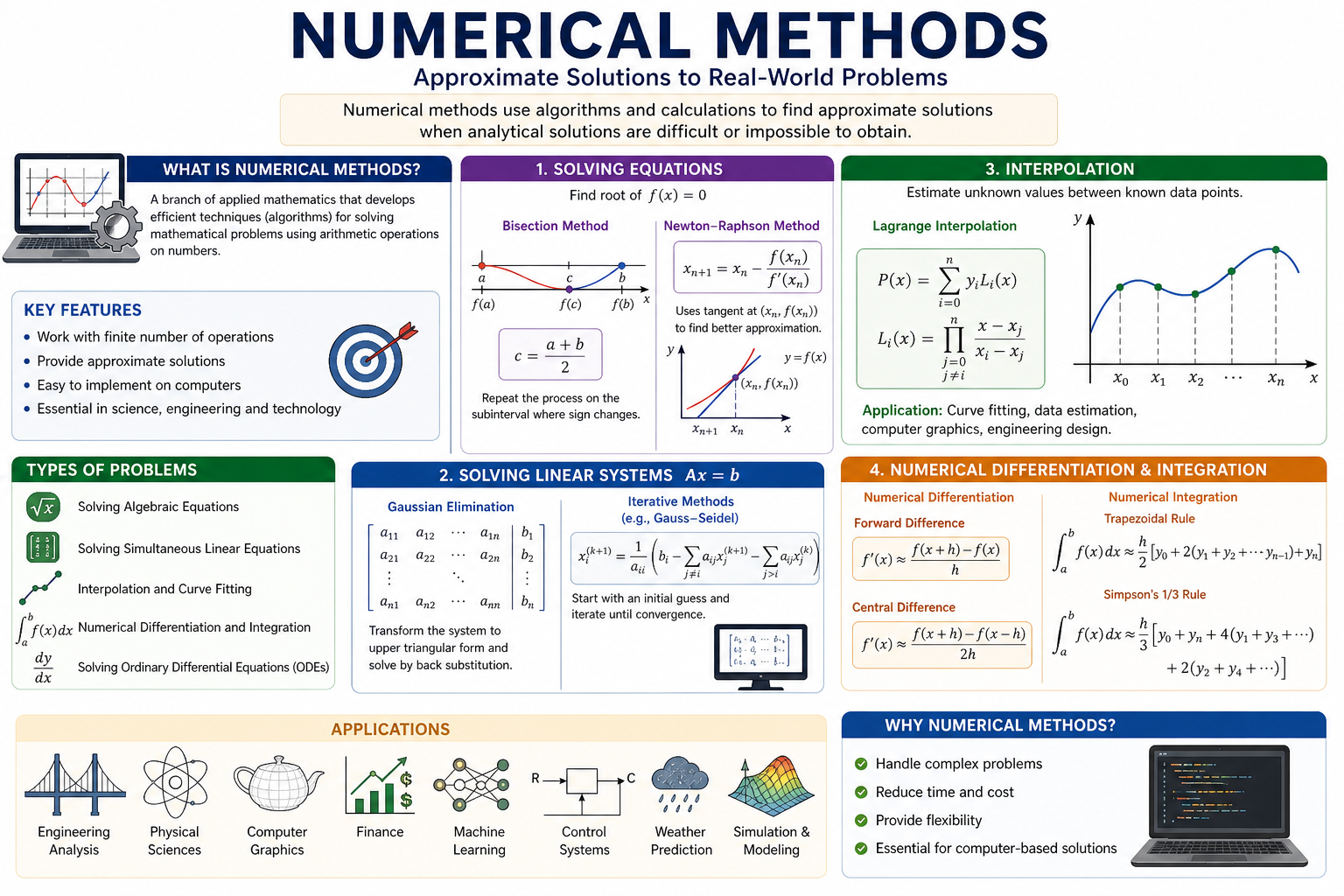

This course introduces the fundamental concepts and techniques of numerical methods, which are used to obtain approximate solutions to mathematical problems that cannot be solved analytically or are too complex for exact solutions. It emphasizes the development of computational algorithms and their implementation in solving real-world engineering and scientific problems.

The course begins with error analysis, including types of errors (absolute, relative, truncation, and rounding errors) and their propagation in numerical computations. It then covers methods for solving nonlinear equations, such as the bisection method, false position method, and Newton–Raphson method.

Next, the course explores techniques for solving systems of linear equations, including Gaussian elimination, LU decomposition, and iterative methods such as Jacobi and Gauss–Seidel methods. Students will also study interpolation and curve fitting, including Lagrange interpolation and Newton’s divided difference method.

Further topics include numerical differentiation and integration, using finite difference formulas and numerical integration techniques such as the trapezoidal rule and Simpson’s rules. The course may also introduce basic numerical methods for solving ordinary differential equations, such as Euler’s method and Runge–Kutta methods.

By the end of the course, students will be able to:

Analyze and control errors in numerical computations

Apply root-finding algorithms to nonlinear equations

Solve systems of linear equations using direct and iterative methods

Perform interpolation and curve fitting for data analysis

Approximate derivatives and integrals using numerical techniques

Implement numerical algorithms to solve engineering problems

This course provides essential computational skills required in engineering, data science, simulation, and scientific computing.

This course introduces the fundamental concepts and techniques of numerical methods, which are used to obtain approximate solutions to mathematical problems that cannot be solved analytically or are too complex for exact solutions. It emphasizes the development of computational algorithms and their implementation in solving real-world engineering and scientific problems.

The course begins with error analysis, including types of errors (absolute, relative, truncation, and rounding errors) and their propagation in numerical computations. It then covers methods for solving nonlinear equations, such as the bisection method, false position method, and Newton–Raphson method.

Next, the course explores techniques for solving systems of linear equations, including Gaussian elimination, LU decomposition, and iterative methods such as Jacobi and Gauss–Seidel methods. Students will also study interpolation and curve fitting, including Lagrange interpolation and Newton’s divided difference method.

Further topics include numerical differentiation and integration, using finite difference formulas and numerical integration techniques such as the trapezoidal rule and Simpson’s rules. The course may also introduce basic numerical methods for solving ordinary differential equations, such as Euler’s method and Runge–Kutta methods.

By the end of the course, students will be able to:

Analyze and control errors in numerical computations

Apply root-finding algorithms to nonlinear equations

Solve systems of linear equations using direct and iterative methods

Perform interpolation and curve fitting for data analysis

Approximate derivatives and integrals using numerical techniques

Implement numerical algorithms to solve engineering problems

This course provides essential computational skills required in engineering, data science, simulation, and scientific computing.

- Teacher: Anwar Ahmad Siddiquee